Image 1 of 1

Image 1 of 1

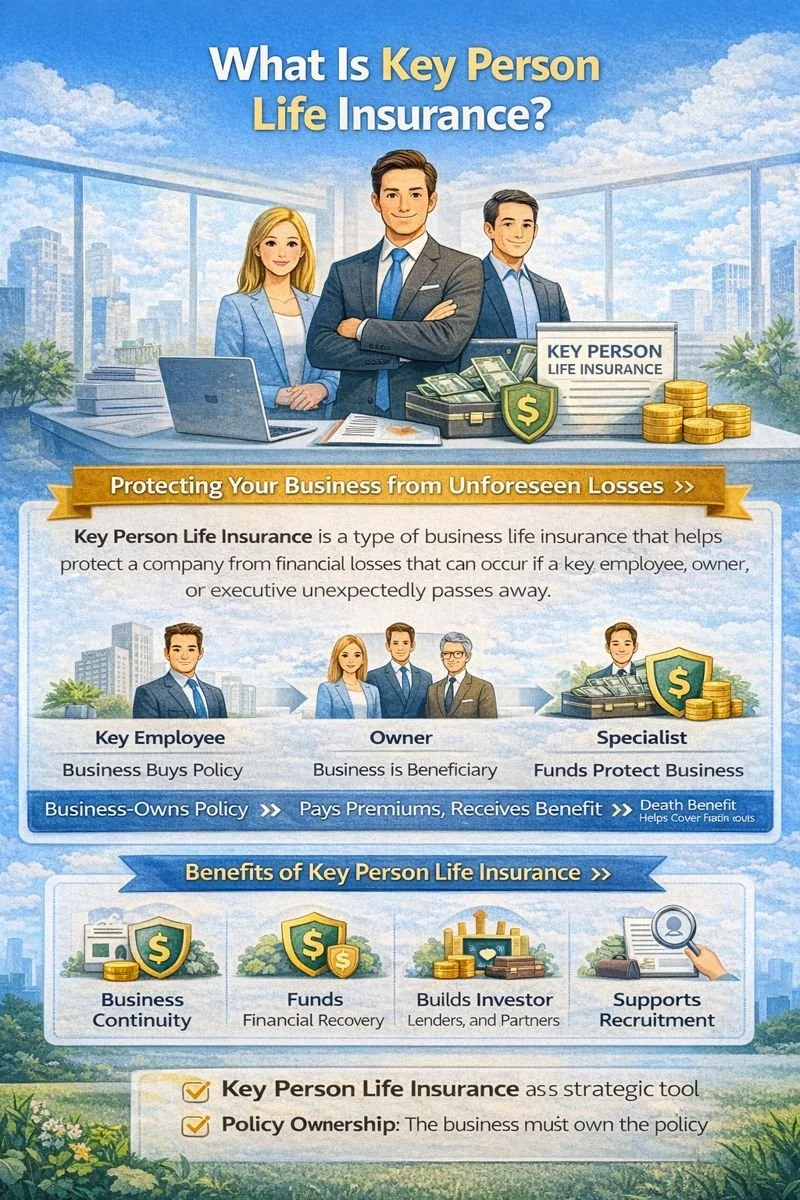

How Key Person Life Insurance Works

The business purchases the policy on the life of the key employee and pays the premiums.

The business is the beneficiary of the policy, meaning the death benefit is paid directly to the company if the key person passes away.

Funds from the policy can be used to cover financial losses, pay off debts, hire a replacement, or maintain business operations.

Key Features of Key Person Life Insurance

Business-Owned Policy

The business owns the insurance and receives the death benefit.

Customizable Coverage

Coverage amounts can be tailored to match the financial impact of losing the key person.

Tax Advantages

Premiums may be tax-deductible, and benefits can provide tax-free financial support to the business.

Flexible Funding Uses

Death benefits can cover lost revenue, recruitment costs, outstanding loans, or operational expenses.

Benefits of Key Person Life Insurance

Protects business continuity during unexpected events

Provides funds to offset financial losses

Supports recruitment and training of replacement personnel

Gives confidence to investors, partners, and employees

Helps safeguard the company’s reputation and client relationships

Considerations

Coverage Limits

It’s important to assess the financial impact of losing a key person to determine adequate coverage.

Policy Ownership

The business must own the policy to ensure the benefit is paid to the company.

Summary

Key Person Life Insurance is a strategic tool for businesses to protect against the financial risk of losing essential employees. By securing this coverage, companies can ensure operational continuity, maintain client confidence, and safeguard revenue streams even in the face of unexpected loss.