Image 1 of 1

Image 1 of 1

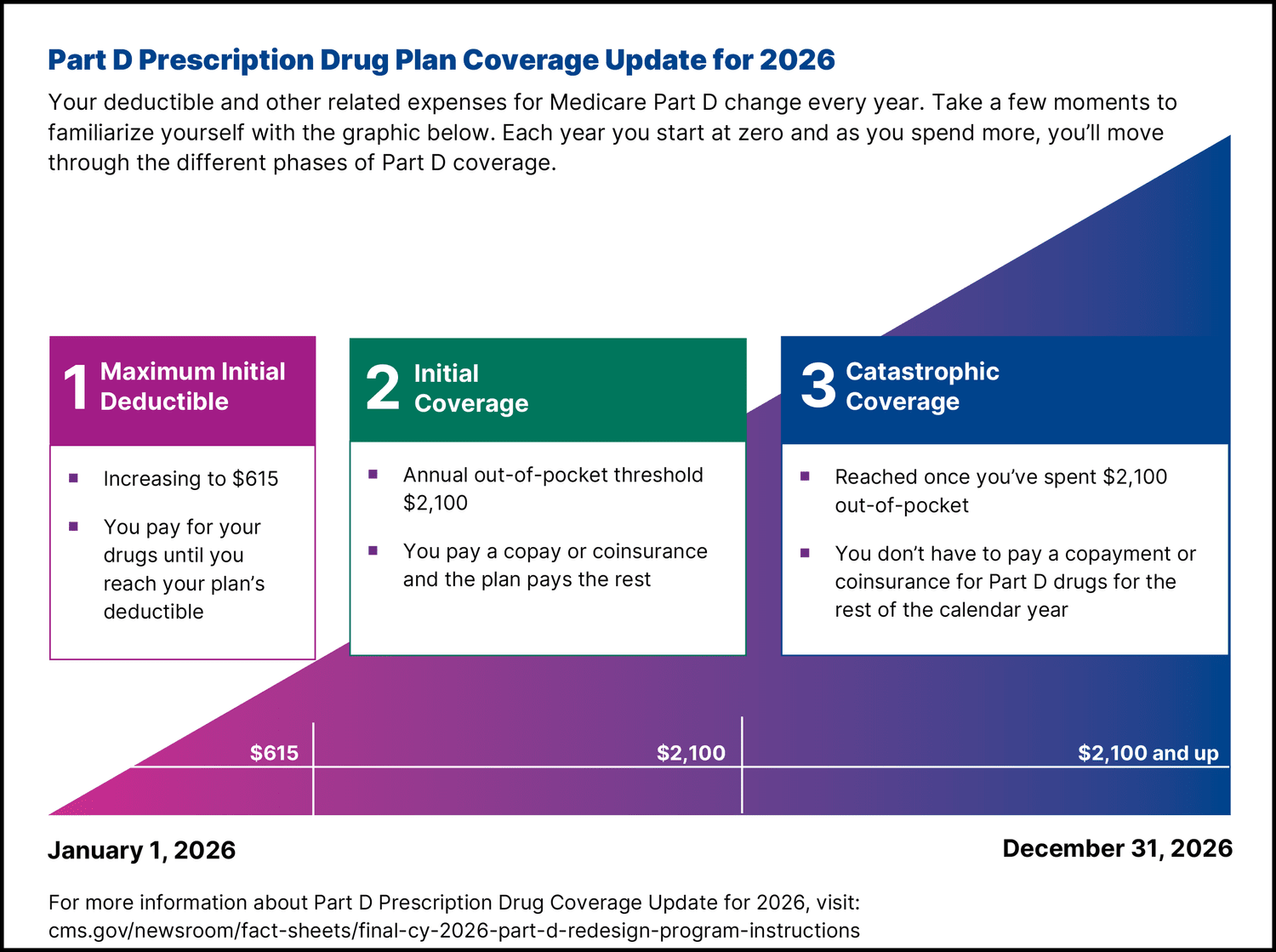

How Part D Works

You enroll in a standalone Part D plan if you have Original Medicare, or your Medicare Advantage plan may include drug coverage.

Each plan has a list of covered drugs (formulary), which can vary by plan.

You typically pay a monthly premium for the plan, plus copayments or coinsurance for medications.

Part D helps protect against high prescription costs by providing structured coverage, including initial coverage, coverage gap, and catastrophic coverage stages.

Key Features of Part D

Wide Drug Coverage

Most Part D plans cover a broad range of prescription medications.

Formularies and Tiers

Drugs are categorized into tiers, which affect your out-of-pocket costs. Generic medications usually cost less than brand-name drugs.

Annual Enrollment

You can enroll, switch, or update your plan during Medicare’s annual enrollment period.

Coverage Gap (“Donut Hole”)

After a certain amount is spent on medications, there may be a coverage gap where you pay higher costs until catastrophic coverage kicks in.

Benefits of Part D

Reduces prescription drug expenses

Offers protection against high medication costs

Access to a wide range of covered medications

Can be combined with Original Medicare or Medicare Advantage

Helps seniors manage chronic conditions affordably

Considerations

Plan Differences

Not all drugs are covered by every plan, so checking your medications against a plan’s formulary is essential.

Premiums and Copays Vary

Costs differ by plan, location, and drug tier.

Late Enrollment Penalty

If you do not enroll when first eligible and go without creditable prescription drug coverage, you may face a permanent late enrollment penalty.

Summary

Medicare Prescription Drug Plans (Part D) help seniors and Medicare beneficiaries manage the cost of prescription medications. Whether as a standalone plan or part of a Medicare Advantage plan, Part D provides valuable financial protection and access to essential medications for maintaining health and well-being.